Exhibit (c)(3)

Strictly Private and Confidential committee materials Allego Transaction Committee | 4 April 2024

Exhibit (c)(3)

Strictly Private and Confidential committee materials Allego Transaction Committee | 4 April 2024

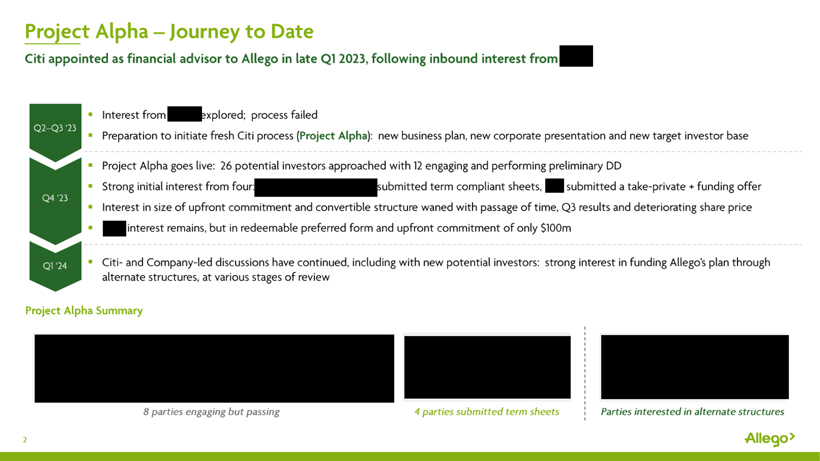

Project Alpha- Journey to Date Citi appointed as financial advisor to Allego in late Ql 2023, following inbound interest from Q2-Q3 ‘23 Interest from explored; process failed Preparation to initiate fresh Citi process (Project Alpha): new business plan, new corporate presentation and new target investor base Q4 ‘23 Project Alpha goes live: 26 potential investors approached with 12 engaging and performing preliminary DD Strong initial interest from four submitted term compliant sheets, submitted a take-private + funding offer Interest in size of upfront commitment and convertible structure waned with passage of time, Q3 results and deteriorating share price interest remains, but in redeemable preferred form and upfront commitment of only $100m Citi- and Company-led discussions have continued, including with new potential investors: strong interest in funding Allego’s plan through alternate structures, at various stages of review Project Alpha Summary 8 parties engaging but passing 4 parties submitted term sheets Parties interested in alternate structures 2

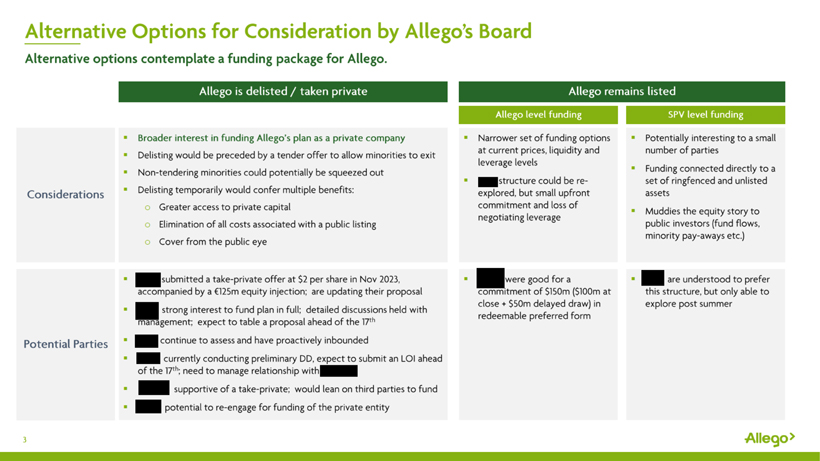

Alternative Options for Consideration by Allego’s Board Alternative options contemplate a funding package for Allego. Allego is delisted / taken private Considerations • Broader interest in funding Allego’s plan as a private company • Delisting would be preceded by a tender offer to allow minorities to exit • Non-tendering minorities could potentially be squeezed out • Delisting temporarily would confer multiple benefits: o Greater access to private capital o Elimination of all costs associated with a public listing o Cover from the public eye Potential Parties • submitted a take-private offer at $2 per share in Nov 2023, accompanied by a • 125m equity injection; are updating their proposal • strong interest to fund plan in full; detailed discussions held with management; expect to table a proposal ahead of the 17th • continue to assess and have proactively inbounded • currently conducting preliminary DD, expect to submit an LOI ahead of the 17th; need to manage relationship with • supportive of a take-private; would lean on third parties to fund • potential to re-engage for funding of the private entity Allego level funding • Narrower set of funding options at current prices, liquidity and leverage levels • structure could be re-explored, but small upfront commitment and loss of negotiating leverage were good for a commitment of $150m ($100m at close + $50m delayed draw) in redeemable preferred form SPV level funding • Potentially interesting to a small number of parties • Funding connected directly to a set of ringfenced and unlisted assets • Muddies the equity story to public investors (fund flows, minority pay-aways etc.) are understood to prefer this structure, but only able to explore post summer Allego> 3

Key Questions for Madeleine • How do you intend to fund the tender offer? Out of which fund and up to what level of acceptances? • Please elaborate on what you mean by credit approved? Do you have an equity commitment letter in place for the required funding? • Do you intend to pursue a squeeze-out of Allego’s minorities post settlement of the tender offer? • How do you intend to support the near term and future funding requirements of the company once delisted / taken private? And over what timeframe? (internal note: Meridiam cite €250m of min equity required in N5Y, and the “willingness to support the procurement of attractive and competitive financing terms” without committing to a funding package themselves) • Are you committed to remaining Allege’s controlling shareholder for the medium to long term? • What is your remaining investment horizon in Allego? • Are you open to ceding outright control of Allego if a competitively priced and full funding package can be sourced? • Have you discussed your proposal with Apollo? When do you intend to do so? Allego> 4