Founded in 2013, Allego is a leading EV charging company in Europe with its first fast charger becoming operational soon after founding and deploying Europe’s first ultra-fast charging station in 2017. From its inception, Allego has focused on EV charging solutions that can be accessed by the highest number of vehicles, regardless of vehicle type or OEM, thus allowing it to grow in a vehicle-agnostic manner.

Allego believes its business is set to expand quickly with the growth of transportation electrification and that its growth could potentially exceed the industry-wide anticipated four-times growth of the number of EVs from 2020 to 2025, according to a report entitled “Electric Vehicle Outlook 2020” by BloombergNEF (“BNEF Report”), a strategic research provider covering global commodity markets and disruptive technologies. The European EV market is larger and growing faster than the U.S. market, according to Allego’s estimates, due to European market attributes that generally favor fast charging, including more stringent regulatory regimes, high urbanization rates, a scarcity of in-home parking in dense cities and significant interurban traffic. According to Allego’s estimates, between 2020 and 2030 fast public charging will increase its share from 24% to 37% of public charging in Europe. The shift from traditional ICE cars to EVs has occurred more rapidly in Europe than expected, particularly in light of governmental regulations such as the total ban of ICE cars in large cities such as London as soon as 2030 and the restrictions on ICE sales in some countries, including the United Kingdom. The BNEF Report projects that the investment in EV charging in Europe for commercial and public charging will require more than $54 billion between 2020 and 2030 and more than an additional $84 billion between 2030 and 2040.

The growth in the EV market in Europe has driven increased demand in public charging. Most of the cars in Europe can only be charged through public charging, as home garage access is often limited. Furthermore, fast and ultra-fast charging sites enable drivers to charge their EV’s in a reasonable time when compared to the time it takes for “fueling” ICE vehicles. EV drivers want to have the same level of service as old “fueling” methods, at a similar price point and Allego seeks to provide that experience.

Allego’s Business Model for EV Charging

Allego’s business model is based on the premise of providing easily accessible, highly reliable, hassle-free charging points to all types of EV users. Allego developed a unique, proprietary software platform that can manage any hardware chargers and charging sessions while enabling any mobile service provider (“MSP”) to use Allego’s network. Allego used this platform to create two complementary business segments to capitalize on the full breadth of EV charging opportunity: its owned fast charging network and high value-add third-party services.

Owned Fast Charging Network

Allego’s primary business focus going forward is in building, owning and operating ultra-fast and fast EV charging sites. Allego is the operator of one of the largest pan-European public EV charging networks. We use our proprietary AllamoTM software to identify premium charging sites and forecast demand using external traffic statistics. These sites generally are situated in high-density urban or suburban locations, and we believe that AllamoTM has been instrumental in securing a strong pipeline of premium sites. Allego’s proprietary software also supports compatibility and an optimized user experience for all EV drivers. The Allego EVCloudTM further provides software solutions for EV charging owners, including payment, analytics, customer support and achieving high uptime. Allego’s charging sites are vehicle-agnostic, and therefore can charge vehicles without limitations on OEM or user groups. Allego is a leader in ultra-fast charging networks in Europe, with 733 fast and 54 ultra-fast charging ports as of June 22, 2021, and intends to accelerate its growth in this business segment.

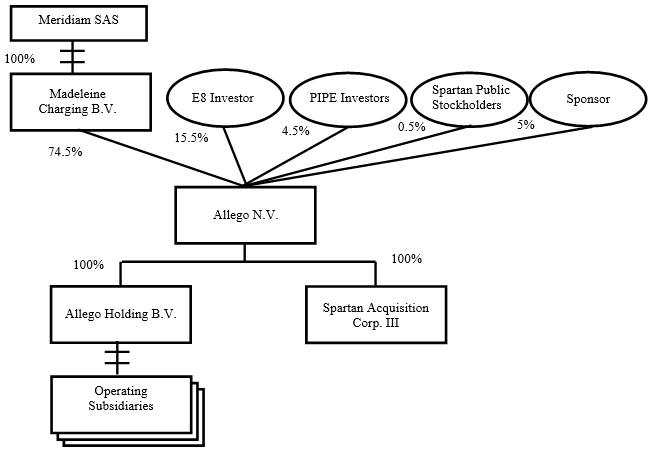

30